Written by: Rutva Patel, a masters student working with

ASU LightWorks on the Digital Carbon Warehouse

Advised by: Todd Taylor, blockchain expert, Thunderbird School of Global Management

A blockchain is essentially a digital ledger of transactions that is duplicated and distributed across the entire network of computer systems on the blockchain.

Okay too many jargons, lets simplify this.

Blockchain is essentially a database that is shared among a network of computers that is secured and hence eliminates the need of “trusted” third parties. Whenever there is an activity (addition/updating), a new block is added to this network which is immutable, or in other words the transaction details cannot be altered, only added to.

“Blockchain technology has long been associated with crypto-currencies such as Bitcoin, but there is so much more that it has to offer, particularly in how public and private organisations secure, share and use data,” comments Steve Davies, global leader for blockchain and partner at PwC UK.

Every time we hear the word Blockchain, there is the word crypto or cryptocurrency associated with it. However, cryptocurrencies such as Bitcoin are actually the first real world application of Blockchain in 2009. A blockchain is a distributed set of data that uses cryptography to verify and secure that information. Rather than having a central database server to store the data, everyone involved in the blockchain has a copy of the information. This enables each involved party to verify that an individual block is accurate using hashing and cryptography. Each block is created from a hash of some information. Anyone who has that same information can create the same hash to verify the block; however, they cannot go backward from the hash to re-create data that makes up the block. Each person updating the blockchain uses a key that verifies that they are who they say they are.

In the above definition we mentioned that “everyone” can be involved in a blockchain, but how do big business get involved in something where their transactions are publicly available? This introduces us to the concept of Public vs Private blockchain.

Let’s dive in and find out the difference between the two.

Public Blockchain is entirely permissionless, meaning anyone can read, write or participate within the blockchain. A Public Blockchain is completely decentralized which means no entity can control the network. Data stored in Public Blockchain is secure as it is not possible to alter the data once it has been validated in the blockchain. Bitcoin and Ethereum are well known examples of a public blockchain.

On the other hand, Private blockchain is permission based and works on the basis of access control and hence restricts people who can participate in the network. In this, only the entities participating in the transaction will have knowledge about it, whereas the others on the network will not be able to access it. A typical example where private blockchain is being used is intra-business can be found in Hyperledger Fabric by Linux foundation.

In the above definition we mentioned that “everyone” can be involved in a blockchain, but how do big business get involved in something where their transactions are publicly available? This introduces us to the concept of Public vs Private blockchain.

Let’s dive in and find out the difference between the two.

In this application a private blockchain will not allow anyone outside the organization to access the data or the transactions taking place in the network. Additionally, because only a few people can access this network the ledger is relatively quick and efficient compared to the public blockchain.

A fun fact, John Wolpert, cofounder of Hyperledger (private blockchain), believes in “stateful internet”. He is a big fan of pushing the management of states in a decentralized manner. John believes that there is an opportunity to use corda’s point to point communication between two parties while being in a “public” blockchain that secures the business rules so that only those two parties have the visibility of the rules.

Recently, Microsoft partnered with JP Morgan Chase on its “private” blockchain products. What started with a Blockchain-as-a-service (Baas) application has now grown into a “sandbox” where companies can test their products with potential customers.

So, Public vs Private Blockchain: Who wins?

The debate is never ending when it comes to public vs private blockchain for various industries. Few people argue that private blockchain defeats the purpose of decentralization, as there is a central authority controlling the nodes of the network. The public blockchain saves money for the company while the private blockchain benefits individuals by giving them anonymity. But we believe that it’s a tradeoff and it depends on business needs.

Let’s see with an example how the public blockchain transaction takes place.

When a new block is added to the blockchain, various nodes in the block are required to execute algorithms to evaluate the history of the blockchain blog. If at least 51% (consensus algorithms) if the nodes authenticate the history and signature of block, then it is accepted to the ledger. There are various consensus algorithms such as Proof of Work (PoW), Proof of Stake (PoS) which provides energy savings and a safer network as attacks become more expensive.

Moving on, there is a new buzz in the air about the term “NFTs”.

It’s crazy to read news of Grimes selling art as NFTs for millions of dollars or the founder of Twitter selling his first tweet. What are NFTs?

In a boring technical sense, NFT or Non-Fungible Token acts like a digital certificate of authenticity. NFTs are cryptocurrencies but unlike fungible cryptocurrencies like bitcoin, they are completely unique. They exist as a string of numbers and letters stored on a blockchain ledger. This information can contain who owns the digital asset, who sold it and when it was sold. This information is also encrypted ensuring NFT’s authenticity and scarcity. If the asset is scarcer, it will be more valuable.

Because of the NFTs there, there is now a space where everyone can be an art collector. The co-founders of the NFT platform have been working to make digital assets more attainable for the general public. They are one of few platforms that allow users to buy NFTs off the site using their credit card.

Along with the supportive hype around the NFTs, some critics have raised concerns around validation of authenticity of the original creator of the digital token. Other than this, mining and trading cryptocurrencies uses up massive amounts of electricity and many artists are beginning to raise an alarm about the ecological costs of the NFTs. Proponents are bullish on the potential for the NFTs but critics are skeptical that it may be a digital bubble in the making.

Are we missing the real benefit of blockchain?

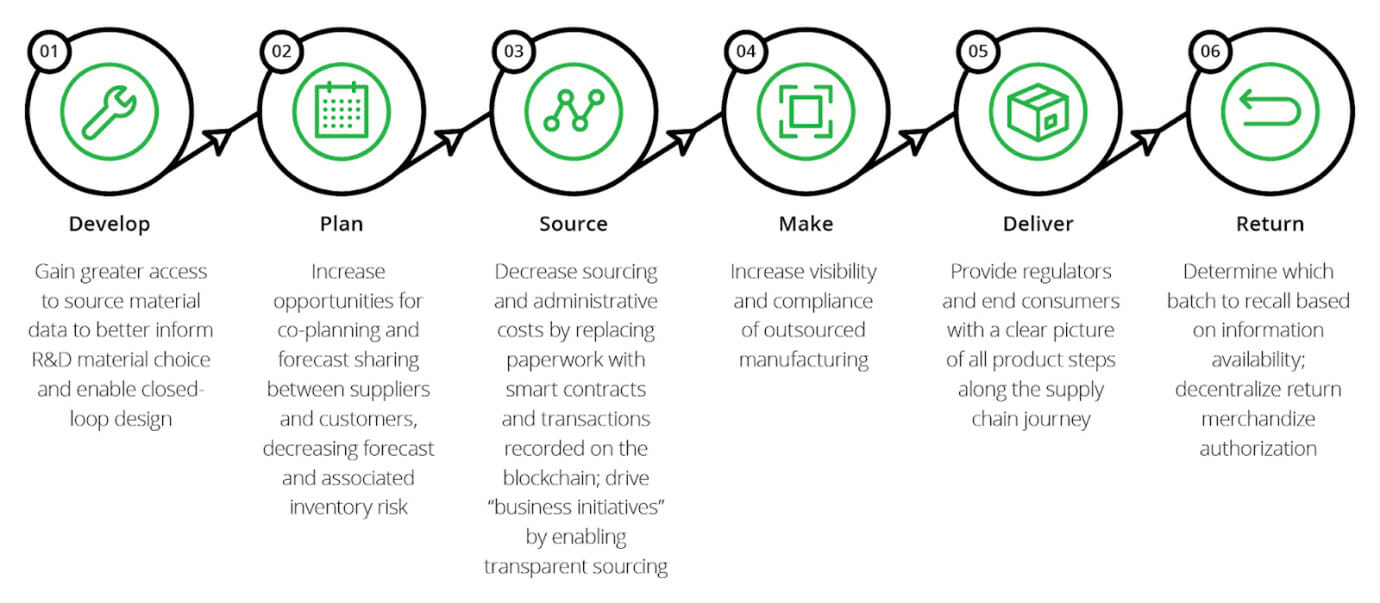

Today, many supply chains in nearly every sector have challenging barriers like complexity, inefficiency, administration and manual processes. As organizations look to Blockchain, for its ability to provide a transformational opportunity for enterprises addressing these challenges, organizational leaders find it to be productive at saving time, and cost, while optimizing efficiency. Blockchain reduces enterprise risk by increasing authenticity, traceability, limiting fraud, reducing over and under stock situations and increasing trust between suppliers, partners, and consumers.

As blockchain gains force, organizations should continue to notice the major parts in their industry that have started exploring different aspects regarding blockchain. Blockchain benefits incredibly from the network effect once a critical mass gathers in a supply chain, it is easier for others to jump on board and gain the benefits. Organizations could focus on different stakeholders in their supply chain and network for indication of timing to develop a blockchain prototype.